Bitcoin price faced a rejection near the crucial resistance, plunging by 2.62% to reach close to $75,000. The rally seems to be driven by geopolitical news, as the recent gains have completely faded. The IRGC fully blocked the Strait of Hormuz again, which has intensified the selling pressure on the token.

After another rejection near the $75K–$78K zone, price action is starting to show signs of exhaustion, not continuation. What makes this setup more concerning is what’s happening beneath the surface. Profit-taking is rising, positioning remains fragile, and the structure continues to print lower highs. This is not a confirmed breakdown yet—but it is no longer a healthy uptrend either.

The current setup increasingly resembles early-stage distribution, where upside attempts weaken, and downside risk quietly builds.

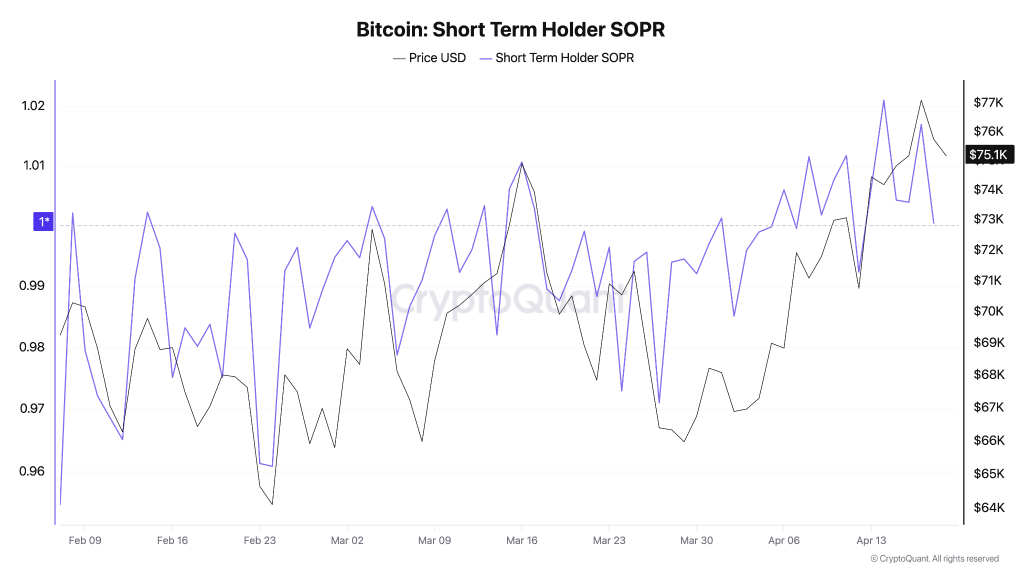

Profit-Taking Rises as Short-Term Holders Turn Active

Short-Term Holder SOPR is now consistently hovering around and above the 1 mark, signaling that recent buyers are actively realizing profits. When SOPR stays above 1, it typically reflects selling into strength rather than holding for higher prices, a behavior often seen during early distribution phases.

However, the data also shows that SOPR is not breaking down below 1 in a sustained way, meaning the market hasn’t entered capitulation yet. Instead, this points to a more controlled environment where participants are gradually offloading positions without panic. In other words, selling pressure is building, but not at a level that confirms a full trend reversal just yet.

Market Remains Indecisive as Long/Short Positioning Stays Mixed

The BTC long/short ratio reflects a market that lacks clear directional conviction. Buy and sell pressure continues to alternate, with no sustained dominance from either side. This kind of imbalance typically signals indecision rather than trend strength, especially when it appears near key resistance levels.

However, occasional spikes in long positioning suggest that traders are still attempting to bet on upside continuation. The problem is timing. When long exposure builds without a confirmed breakout, it often creates a vulnerable setup where even a small downside move can trigger liquidations. For now, the data doesn’t show extreme crowding, but it does highlight a market that is fragile, reactive, and prone to sudden volatility rather than stable continuation.

BTC Faces Rejection as Downtrend Structure Holds

Bitcoin’s price action continues to respect a clear descending trendline, with the latest move once again rejecting near the $75K–$78K resistance zone. This marks another lower high, reinforcing the broader downtrend that has been in place since the previous peak.

While the recent bounce from the $60K–$65K region shows buyers are still active at lower levels, the inability to break above resistance keeps the structure weak. As long as Bitcoin price remains below this trendline, the path of least resistance leans downward.

From here, the key level to watch sits near the $70K zone. A sustained move below this area could expose BTC to a deeper correction toward the $60K–$55K range. On the upside, bulls need a decisive breakout above $78K to invalidate the current structure and shift momentum back in their favor.

What’s Next for the BTC Price Rally?

The Bitcoin price is not breaking down yet, but the structure is no longer supportive of upside continuation. With repeated rejections at resistance, rising profit-taking, and fragile positioning, the market is starting to tilt toward a liquidity-driven move rather than a sustained rally. This is the kind of setup where late longs get trapped, and volatility expands quickly.

Unless the BTC price reclaims the $78K zone with strong confirmation, the current structure favors a move lower, with $70K acting as the first key test. A breakdown below this level could accelerate downside toward the $60K–$55K region.